Insurance Requirements in Commercial Leases: The Hidden Costs and How to Negotiate Coverage Obligations That Actually Fit Your Business

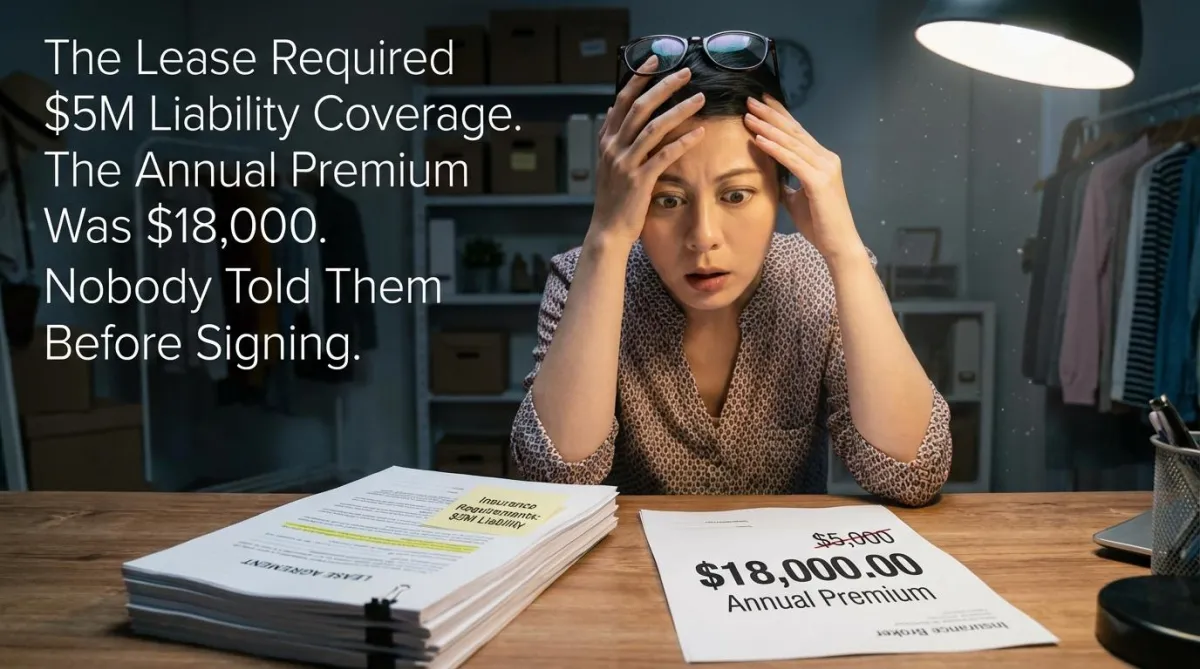

A small retail tenant signed a lease requiring commercial general liability insurance with $5 million per occurrence limits, a $10 million umbrella policy, and a waiver of subrogation. The tenant’s broker quoted the required coverage at $18,000 annually — more than three times what similar coverage cost at their previous location, where the lease required $1 million per occurrence.

The insurance requirement added $1,500 per month to the tenant’s effective occupancy cost. It wasn’t disclosed in the LOI, wasn’t estimated in the financial model, and wasn’t negotiated before signing. The lease language simply stated the requirement. The cost was the tenant’s problem.

Commercial lease insurance requirements are a hidden occupancy cost that most tenants don’t model until they’re shopping for coverage. The landlord sets the requirements to protect the property and minimize their own insurance exposure. The tenant bears the cost of meeting those requirements.

If you want to know what your lease requires in insurance coverage, run it through sasir.ai — the first scan is free.

What Commercial Leases Typically Require

Most commercial leases require the tenant to carry some combination of:

Commercial general liability (CGL): covers bodily injury and property damage claims arising from the tenant’s operations. Typical commercial lease requirements range from $1 million to $5 million per occurrence, sometimes with an umbrella requirement on top.

Property insurance: covers the tenant’s personal property, equipment, and improvements (often required on a replacement cost basis).

Business interruption insurance: covers lost income if the tenant’s operations are interrupted by a covered event.

Workers’ compensation: required by law in most states but often explicitly required in the lease as well.

Waiver of subrogation: a provision requiring the tenant’s insurer to waive its right to pursue claims against the landlord for damages covered by the tenant’s policy. This prevents the tenant’s insurer from suing the landlord after paying a claim.

What to Check and Negotiate

Verify the required coverage limits before signing: ask your insurance broker to quote the required coverage from the lease before agreeing to the lease. The annual premium is part of the total occupancy cost calculation.

Negotiate coverage limits appropriate to your business size and risk: a $5 million per occurrence requirement may be appropriate for a high-traffic restaurant but disproportionate for a small office tenant. Coverage limits should reflect actual risk.

Confirm the landlord’s insurance obligations: the lease should specify what insurance the landlord carries on the building. If the landlord’s coverage is inadequate, the tenant may face exposure even with their own required coverage.

Understand the waiver of subrogation: ensure both parties waive subrogation against each other on a mutual basis — not just the tenant waiving against the landlord.

Request an annual right to update the insurance requirement: as business size and operations change, the required coverage should be revisable — not locked at a level that was either too high or too low at signing.

The Bottom Line

Insurance requirements in a commercial lease are a real cost that belongs in the total occupancy cost calculation. Get a coverage quote before signing. Negotiate limits proportionate to your business. And make sure the waiver of subrogation is mutual.

Related resources:

Run your lease through sasir.ai. First scan is free.