Personal Guarantees in Franchise Leases: Why the Risk Is Bigger Than You Think — and What to Negotiate

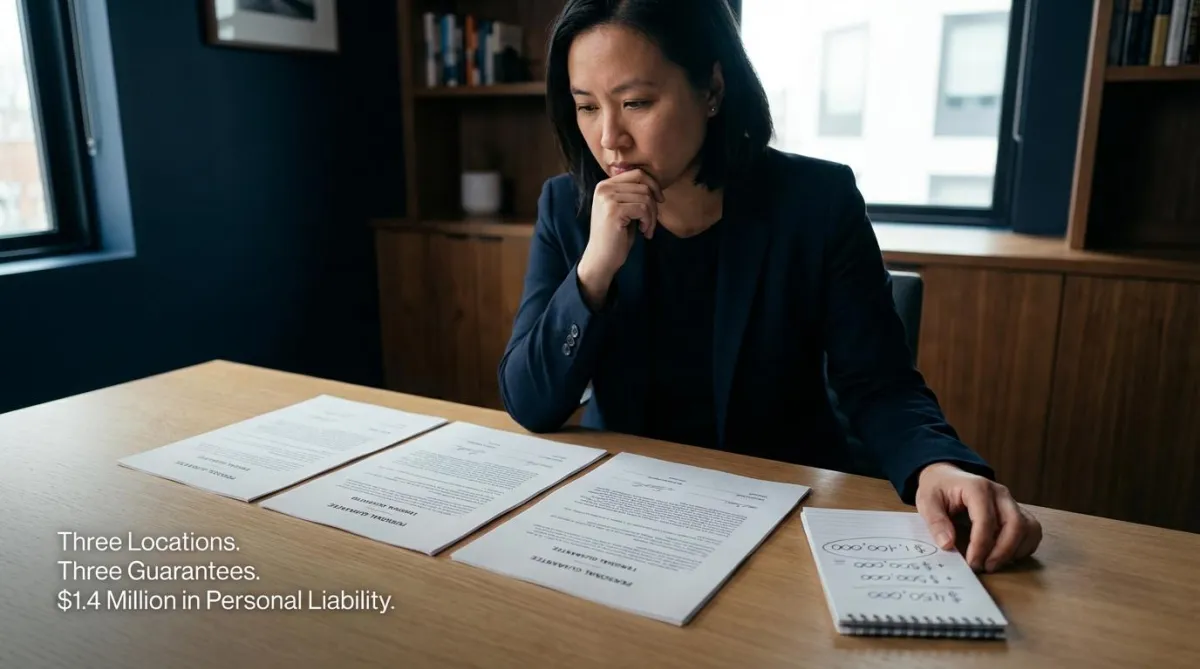

A multi-unit fitness franchisee had signed personal guarantees on three leases — her two operating locations and a third she was opening. Each guarantee was unlimited. Each was for the full remaining lease term. None had a burn-off provision or a cap.

When she sat down to calculate her total personal liability, the number was $1.4 million. That was the combined remaining rent obligation across all three leases, guaranteed personally, with no reduction for performance, no release on sale, and no expiration until the leases did.

She hadn’t thought about it in aggregate. She’d signed each guarantee as it came, location by location, the way the franchise system expected. Nobody had told her the exposure was stacking.

Personal guarantees in franchise leases are standard — and the franchise context makes them more dangerous than the general commercial lease version. The stacking problem, the spousal liability risk, the survival of the guarantee after franchise sale, and the absence of any burn-off or cap in most franchisee-signed leases create a personal financial exposure profile that most franchisees don’t fully understand until they’re already in it.

This post explains how personal guarantees work specifically in franchise leases, where the franchise-specific risks amplify the standard guarantee problems, and the levers franchisees have to negotiate before signing each location.

If you want to know exactly how your franchise lease’s personal guarantee is structured, run it through sasir.ai — our AI-powered lease analysis tool. The first scan is free.

How Franchise Personal Guarantees Differ From Standard Ones

In any commercial lease, a personal guarantee makes the individual signer personally liable for the business’s lease obligations if the business entity cannot perform. It pierces the corporate shield. If the LLC defaults, the landlord comes after the individual.

In a franchise context, the personal guarantee carries additional risk layers that independent tenants don’t face:

Stacking across multiple units. A franchisee who grows to two, three, or four locations signs a personal guarantee at each. These guarantees are typically independent documents with no cross-reference or aggregate cap. The franchisee’s total personal exposure is the sum of all remaining lease obligations across all locations. Most franchisees calculate their exposure per location. They should be calculating it in aggregate.

No burn-off aligned to performance. General commercial leases increasingly include guarantee burn-off provisions that reduce the guarantor’s exposure after a period of timely payment — say, 24 to 36 months of clean performance reduces the guarantee to twelve months of base rent. In franchise leases where the franchisor has pre-negotiated the lease form or where the landlord has leverage from the site approval dynamic, these burn-off provisions are frequently absent. The guarantee stays flat regardless of how well the business performs.

Survival after franchise sale. When a franchisee sells their franchise, the buyer typically assumes the lease and the new personal guarantee obligation. But the seller’s guarantee in many leases continues to be in force unless explicitly released by the landlord. A franchisee who sold a location two years ago may still be personally guaranteeing a lease on a business they no longer own or operate, while the buyer’s guarantee sits alongside theirs.

Spousal liability. Many commercial lease guarantees require the guarantor’s spouse to co-sign if the guarantor is married. This extends the personal liability into the household — joint assets, not just business assets, become part of the guarantee exposure. This is particularly impactful when one spouse is the franchisee and the other has a professional career or assets that are independent of the franchise.

The franchise personal guarantee problem is not just about the size of any single guarantee. It’s about the accumulation of guarantees across locations, the absence of burn-off mechanisms, the survival risk after sale, and the extension of liability into the household. Most franchisees discover this in aggregate for the first time when they’re trying to expand, sell, or exit.

The Stacking Problem in Detail

Here is how the stacking calculation works for a three-unit franchisee:

Location 1: 7-year lease, 4 years remaining, $5,500/month base rent = $264,000 guaranteed

Location 2: 5-year lease, 3 years remaining, $4,800/month base rent = $172,800 guaranteed

Location 3: 7-year lease, 7 years remaining (new location), $6,200/month base rent = $520,800 guaranteed

Total personal guarantee exposure: $957,600. If rent acceleration applies on default — meaning all remaining rent becomes immediately due — that exposure is callable in a single event, not amortized over the remaining terms.

Most franchisees with three units don’t walk around with the number $957,600 in their heads as their personal liability. They think of each location individually. The aggregate is the number that matters.

The Spousal Liability Problem

If the lease guarantee requires spousal co-signature, both spouses are personally liable. This has several practical consequences:

Community property exposure: in community property states (California, Texas, Arizona, Nevada, and others), community assets may be reachable regardless of whether the spouse co-signed, depending on how the guarantee is structured

Professional license risk: if the non-franchisee spouse holds a professional license (medical, legal, financial), a judgment on a lease guarantee can affect their professional standing and future earning capacity

Divorce complexity: if the spouses separate, the guarantee obligation doesn’t divide cleanly — both parties remain jointly and severally liable until the lease expires or the landlord releases one

What to negotiate: push hard to remove the spousal co-signature requirement. Most landlords include it as a default because it maximizes their recovery options — but it is negotiable, particularly when the franchisee has demonstrated creditworthiness or operating history. If the landlord insists, negotiate that the spouse’s liability is limited to a defined cap (e.g., six months of base rent) rather than unlimited joint liability.

The Survival Problem: Guaranteeing a Business You No Longer Own

When a franchisee sells their franchise, the standard expectation is that the buyer assumes the lease and the seller is released. In practice, many franchise lease guarantees do not provide automatic release on assignment. The seller’s guarantee remains in force until the landlord affirmatively releases it — and landlords have no obligation to release it unless the lease requires them to.

The result: the selling franchisee remains personally liable for a lease on a business they don’t control, operated by a buyer whose financial strength they have no visibility into, for a term they have no ability to manage.

This is not a theoretical risk. It is a common outcome in franchise transfers where the release was not negotiated at the time of the original lease signing. The franchisee who sold three years ago and assumed their liability ended with the sale may find that assumption was wrong.

What to negotiate: include an explicit guarantee release provision tied to qualified assignment. Language: ‘Guarantor shall be released from all obligations under this Guarantee upon the landlord’s approval of an assignment of this Lease to an assignee who meets Landlord’s reasonable financial standards, which approval shall not be unreasonably withheld.’ This provision should be in the original lease, not negotiated at the time of sale when leverage is lowest.

Negotiate the release provision before you sign the lease. At the time of franchise sale, the landlord has maximum leverage and minimum incentive to release a guarantor who is still financially solvent. The time to secure the release right is before the landlord needs anything from you.

What to Negotiate: The Franchise-Specific Guarantee Framework

The four components of a well-negotiated franchise personal guarantee:

1. Performance-based burn-off. The guarantee reduces after a defined period of clean performance. Structure: unlimited guarantee for the first 24 months, reduces to 12 months of base rent after 24 consecutive months of timely payment, reduces to 6 months after 48 months. This rewards the franchisee’s operating track record with reduced personal exposure.

2. Cap per unit. For multi-unit franchisees, negotiate a cap on each guarantee rather than unlimited exposure. A cap of 12 to 18 months of base rent per location converts open-ended stacking liability into defined, manageable risk. The aggregate across locations is still meaningful — but it’s a number you can calculate and plan around.

3. Release on qualified assignment. The guarantee terminates automatically when the lease is assigned to a buyer who meets landlord’s reasonable financial standards, without requiring separate landlord approval of the release. Build this into the original lease as a defined right, not a request at the time of sale.

4. Spousal carve-out or cap. Remove the spousal co-signature requirement, or limit the spouse’s liability to a defined cap separate from the franchisee’s guarantee. This protects household assets that are independent of the franchise and removes household liability from the guarantee’s scope.

Before You Sign: The Franchise Guarantee Audit

Before signing any personal guarantee on a franchise lease, answer these questions:

What is the total guarantee exposure on this location (remaining term × monthly rent)?

What is my aggregate guarantee exposure across all current and proposed locations?

Does the guarantee have a burn-off provision? If not, is one negotiable?

Does the guarantee have a cap? If not, is a cap negotiable?

Does the guarantee include a release on qualified assignment? If not, how do I exit?

Does the guarantee require spousal co-signature? Can this be removed or capped?

Does the guarantee contain a survival clause that extends liability beyond lease expiration?

If rent acceleration applies on default, what is the maximum callable amount in a single event?

These are not hypothetical questions. For a franchisee with multiple locations and an unlimited guarantee on each, the answers define the total personal financial risk of the franchise portfolio.

The Bottom Line

Personal guarantees in franchise leases are expected, standard, and rarely fully understood in aggregate. A franchisee growing from one unit to three signs three guarantees — each presented as a routine lease requirement, each with no individual burn-off or cap, each surviving the franchise sale unless the release was negotiated at signing.

The burn-off, the cap, the qualified assignment release, and the spousal carve-out are the four provisions that convert an open-ended personal liability into a defined and manageable risk. Negotiate all four before signing each location. The aggregate exposure depends on it.

Related resources:

How to Negotiate Your Personal Guarantee in a Commercial Lease

The Franchise Lease Trap: Why Franchisees Face Lease Risks That Independent Tenants Don’t

If you want to know exactly how your franchise lease’s personal guarantee is structured, run it through sasir.ai. The first scan is free.